I couldn’t get the money back until I was 55 at the earliest. And that felt scary. What if I needed it? What if something happened? What if I wanted to use it for something important?

So instead, I did the sensible thing. I invested into an ISA. Accessible, flexible, mine whenever I wanted it.

And then I spent it.

Not all at once, not recklessly — just gradually, over time, the way accessible money tends to disappear. A holiday here, a gap in income there, a sensible-at-the-time purchase that I’ve long forgotten. The ISA did exactly what it was designed to do: it gave me access to my money. And that was the problem.

The thing I got completely backwards

I thought the restriction of a SIPP was a downside. Turns out it was the whole point.

The money I lock away in my SIPP can’t be touched until I’m 55 (rising to 57 by 2028). I can’t spend it on a whim. I can’t dip into it during a slow month. I can’t convince myself I’ll replace it later. It just sits there, quietly compounding, completely protected from the thing most likely to derail my retirement savings — which is me.

Accessible money is spendable money. For a lot of us, those two things are the same thing. A SIPP removes the temptation entirely — and that’s not a bug, it’s the feature.

Once I understood that, the “restriction” stopped feeling like a loss and started feeling like a gift.

Then I discovered the actual free money

I’d vaguely heard about pension tax relief before but never really understood it. Then I made my first SIPP contribution through Interactive Investor and got a notification I wasn’t expecting:

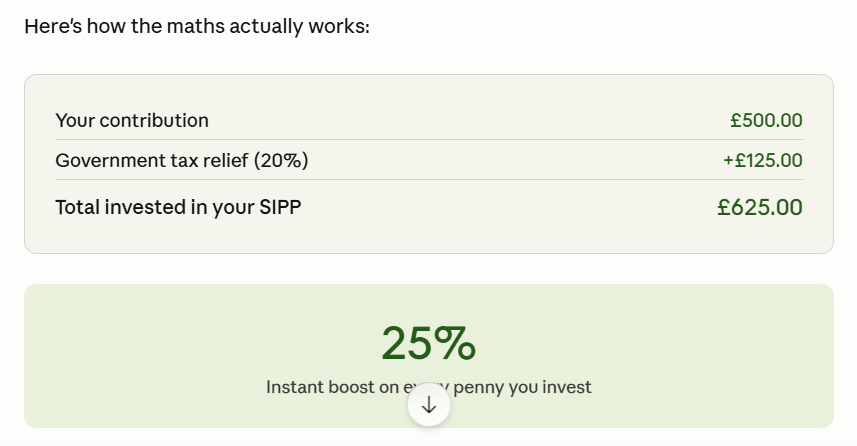

“II will reclaim and invest an extra £125 on your behalf. This usually takes 4–8 weeks, so your total investment will be £625.”

I’d put in £500. The government was sending me £125 for free. No forms, no waiting on hold, no faff — Interactive Investor claims it from HMRC on my behalf and drops it straight into my account.

Here’s how the maths actually works:

Your contribution

£500.00

Government tax relief (20%)

+£125.00

Total invested in your SIPP

£625.00

25%

Instant boost on every penny you invest

Your £500 becomes £625 the moment the relief lands. Before it’s even had a chance to grow. That’s a 25% instant return before any investment growth at all — which is something no ISA, no stocks and shares account, nothing else can offer you from day one.

What if you pay higher rate tax?

If you’re a higher rate (40%) or additional rate (45%) taxpayer, you get even more relief — but the extra portion above basic rate has to be claimed yourself via a Self Assessment tax return. Interactive Investor automatically claims the basic 20% for you, but the additional relief won’t just appear. Worth knowing, and worth doing.

The cost of waiting

Here’s the part that stings a little when I think about it too long: compound growth needs time. Every year I spent investing into an ISA and then spending it was a year my pension missed out — not just on the contributions, but on the growth those contributions would have generated, and the growth on that growth, year after year.

That lost time can’t be bought back. All I can do is start properly now.

If you’ve been putting off your pension for the same reasons I did — the accessibility thing, the “I’ll sort it later” thing, the vague sense that it’s complicated — I get it. I really do. But later is more expensive than you think. And the tax relief makes starting now feel a lot less painful.

The government is literally handing you free money to do it. That’s not nothing.

Delete the ISA habit. Start the SIPP. Future you will be very glad you did.

Formatting ideas: