I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.

I have never been a Hargreaves Lansdown customer.

I chose Interactive Investor seven years ago after researching both platforms and I have never looked back. But when I decided to write this review, I wanted to do it properly. Not a quick scan of the homepage and a summary of the headline fee. Properly.

So I went back to HL’s website with fresh eyes and spent time across eight separate pages piecing together the full fee picture, because no single page gives you everything you will actually pay. I built the complete fee table myself from scratch. Then I analysed the most recent Trustpilot reviews, mapped the sentiment month by month, and looked for patterns in the complaints.

What I found was a story about a significant ownership change, a fee restructure framed as good news that many customers experienced as the opposite, and a Trustpilot score in visible decline. The data in this Hargreaves Lansdown review tells a clear story. Here it is.

Table of Contents

Quick Verdict

Best for: investors who prioritise phone based customer support and want a well known brand behind their pension, particularly those earlier in their journey who may need reassurance through unfamiliar processes.

Not for: long term ISA and SIPP holders building larger portfolios where HL’s percentage based fees compound significantly over time. At portfolio sizes above roughly £50,000 across ISA and SIPP combined, flat fee platforms become materially cheaper.

Overall: HL remains a credible, FCA regulated platform with genuine strengths in customer accessibility. But the March 2026 fee restructure and the ongoing private equity transition mean it deserves more scrutiny than its brand reputation alone would suggest.

What Is Hargreaves Lansdown?

Hargreaves Lansdown is the UK’s largest retail investment platform. Founded in Bristol in 1981 by Peter Hargreaves and Stephen Lansdown, it grew over more than four decades into a business managing over £172 billion for more than two million clients. It is fully regulated by the Financial Conduct Authority and your investments are protected by the Financial Services Compensation Scheme up to £85,000.

Like Interactive Investor, it is a self directed platform. It does not tell you what to invest in or manage your money on your behalf. The decisions are yours. What it provides is the infrastructure, the account types, the research tools, the educational resources, and the customer support to help you make those decisions with confidence.

What changed in March 2025

In August 2024, HL’s board agreed to a £5.4 billion takeover by a consortium of three organisations: CVC Capital Partners, a global private equity firm; Nordic Capital, a Swedish private equity investor; and the Abu Dhabi Investment Authority, a sovereign wealth fund owned by the government of Abu Dhabi. The deal completed on 25 March 2025, at which point HL was delisted from the London Stock Exchange and re-registered as a private limited company.

On the day the deal completed, the entire existing board resigned and a new board was installed. Co-founder Peter Hargreaves retained a 14% shareholding but stepped down from the board in October 2025, nominating his son Robert as his replacement.

The buyers were explicit from the outset: a technology led transformation and a restructuring of the business to drive future growth. Twelve months later, the first major fee restructure in over a decade arrived. The connection between the two events is not speculation. It is the timeline.

HL is no longer a founder led, publicly accountable British company. It is now owned by private equity. That is not a reason to avoid it, but it is relevant information for anyone making a long term decision about where to hold their pension.

Fees: The Complete Picture in One Place

To build a complete picture of what you will actually pay, I had to open eight separate pages of HL’s website and collate the information myself. There is no single page that shows you everything. That is worth naming, because transparency about fees is one of the most important things a platform can offer someone who is newer to investing.

So here is everything in one place.

Full fee table: all account types

| Account | Annual charge (funds) | Annual charge (shares/ETFs) | Shares cap (month) | Fund trade | Share trade | Phone dealing |

|---|---|---|---|---|---|---|

| Fund and Share Account | 0.35% | 0.35% | £12.50 | £1.95 | £6.95 | £29 |

| Stocks and Shares ISA | 0.35% | 0.35% | £12.50 | £1.95 | £6.95 | £29 |

| Lifetime ISA | 0.25% | 0.25% | £3.75 | £1.95 | £6.95 | £29 |

| SIPP | 0.35% | 0.35% | £12.50 | £1.95 | £6.95 | £29 |

| SIPP Drawdown | 0.35% | 0.35% | £12.50 | £1.95 | £6.95 | £29 |

| Junior ISA | Free | Free | Free | Free | Free | £29 |

| Junior SIPP | 0.35% | 0.35% | £12.50 | £1.95 | £3.95 | £29 |

| Bare Trust Account | 0.35% | 0.35% | £12.50 | £1.95 | £6.95 | £29 |

Monthly regular investing via Direct Debit is free across all account types. Government stamp duty of 0.5% applies separately to UK share purchases.

Tiered annual charges

HL’s percentage fee reduces as your portfolio grows, but the tiers apply per account, not across your combined holdings. If you hold a SIPP and an ISA, each is assessed independently. This matters more than it might initially appear.

| Portfolio value (per account) | Annual charge |

|---|---|

| Up to £250,000 | 0.35% |

| £250,000 to £1,000,000 | 0.25% |

| £1,000,000 to £2,000,000 | 0.10% |

| Over £2,000,000 | No charge |

What the percentage fee actually costs you

Here is where the flat fee versus percentage fee conversation becomes concrete. These are the real annual costs of HL’s 0.35% charge at three portfolio sizes, compared directly with Interactive Investor’s flat monthly fee.

| Portfolio size | HL annual cost (0.35%) | Interactive Investor annual cost |

|---|---|---|

| £50,000 | £175.00 | £179.88 (Plus plan) |

| £77,000 | £269.50 | £179.88 (Plus plan) |

| £100,000 | £350.00 | £179.88 (Plus plan) |

At £50,000, the two platforms are broadly comparable. Above that, every additional pound in your portfolio costs you more with HL and nothing more with Interactive Investor. At £77,000 the gap is already £89.62 per year. At £100,000 it is £170.12. And it keeps growing.

For a woman building both an ISA and a SIPP simultaneously, this fee gap compounds across two accounts every single year.

Fees correct as of June 2026. Always verify current charges directly on HL’s website before making any decisions.

The March 2026 Fee Restructure: What Actually Happened

In January 2026, HL announced its first major fee restructure in over a decade. The headline was a reduction. The reality, for a significant proportion of existing customers, was an increase.

What HL said: the main platform fee was reduced from 0.45% to 0.35% for portfolios under £250,000. HL stated that around 80% of existing customers would pay less or about the same.

What customers experienced:

The ISA annual fee cap rose from £45 to £150. AJ Bell’s ISA cap remains £42. For ISA holders who had previously benefited from the £45 ceiling, this was not a reduction. It was more than a trebling of the maximum annual charge on that account.

Funds, previously free to trade, now incur a £1.95 dealing charge per transaction. For investors who rebalance regularly or invest monthly into multiple funds manually, this is a new and recurring cost that did not exist before.

The Fund and Share Account, which previously attracted no platform charge for holding shares, now carries a 0.35% annual fee capped at £150 per year. Investors holding shares outside tax wrappers saw a charge introduced where none previously existed.

The human cost came through clearly in the Trustpilot data. One reviewer saw their monthly cost rise from £3.04 to £10.33, an increase of £87 per year. Another described their ISA fees as having tripled overnight. Multiple reviewers, some with relationships with HL stretching back ten, fifteen and twenty years, described feeling deliberately misled by the framing of the announcement.

The complaint here goes beyond the numbers. The recurring theme is not simply “my fees went up.” It is “I was told my fees were going down and then my fees went up.” That describes a breakdown in trust, not just a pricing disagreement.

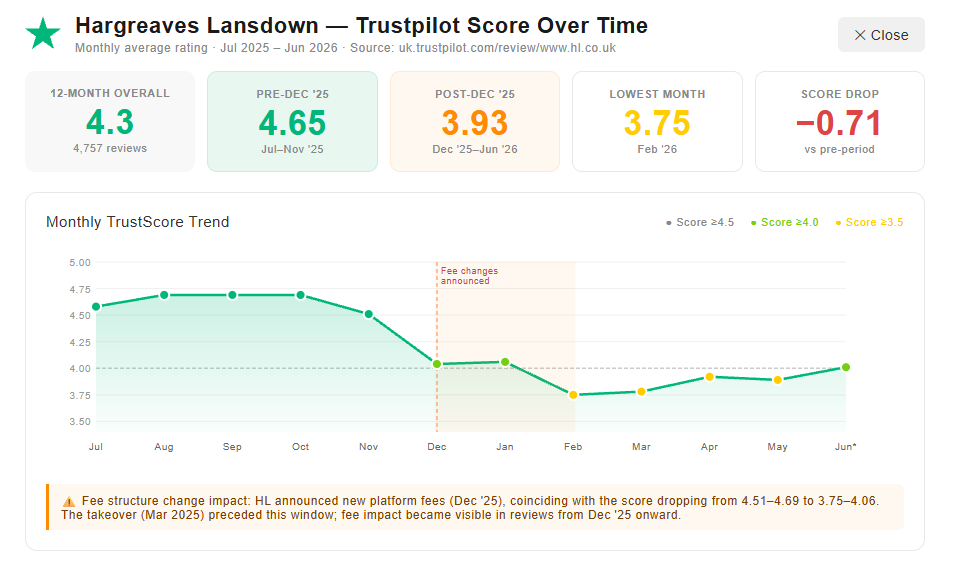

The Trustpilot Story: What the Data Actually Shows

HL’s overall Trustpilot score is 4.3 out of 5 from over 20,000 reviews. That sounds reassuring. But that number is an average across years of reviews, and averages hide the direction of travel.

When you look at the monthly data, a very different picture emerges.

Monthly Trustpilot scores: July 2025 to June 2026

| Month | Average score | Reviews | 5 star % | 1 star % |

|---|---|---|---|---|

| Jul ’25 | 4.58 | 701 | 75% | 3% |

| Aug ’25 | 4.69 | 680 | 82% | 2% |

| Sep ’25 | 4.69 | 665 | 86% | 4% |

| Oct ’25 | 4.69 | 779 | 86% | 4% |

| Nov ’25 | 4.51 | 337 | 81% | 8% |

| Dec ’25 | 4.04 | 282 | 48% | 9% |

| Jan ’26 | 4.06 | 324 | 59% | 13% |

| Feb ’26 | 3.75 | 216 | 55% | 23% |

| Mar ’26 | 3.78 | 237 | 53% | 19% |

| Apr ’26 | 3.92 | 194 | 61% | 18% |

| May ’26 | 3.89 | 173 | 57% | 17% |

| Jun ’26 | 4.01 | 169 | 62% | 14% |

Source: Trustpilot, https://uk.trustpilot.com/review/www.hl.co.uk/transparency, accessed June 2026.

From July to November 2025, HL was a platform its customers were genuinely happy with. Scores ran consistently between 4.51 and 4.69. Five star reviews accounted for 75% to 86% of all reviews each month.

Then in December 2025, the fee changes were announced. Not implemented. Announced.

In a single month, the average score dropped from 4.51 to 4.04. The five star share collapsed from 81% to 48%. By February 2026, the score hit its lowest point of 3.75. One star reviews reached 23% of all reviews that month, more than five times the pre-announcement level. Nearly one in four people leaving a review gave HL the lowest possible rating.

One thing I want to be honest about: when I read the December reviews directly, the complaints were not all about fees. Operational failures were already generating significant negative sentiment at the same point. The fee announcement and a deterioration in operational performance appear to have arrived together, and the data reflects both.

The platform is recovering. By June 2026 the score had climbed back to 4.01. But the one star rate remains at 14%, still three to four times higher than before December 2025.

The Three Most Common Complaints

1. Transfers, withdrawals and account administration

This is the dominant complaint category by some distance, and it has been running long enough to represent a systemic issue rather than isolated incidents.

Outbound ISA and stock transfers are taking eight to twelve weeks with no proactive updates. SIPP drawdown requests are delayed by weeks. Account lockouts are blocking withdrawals while deposits into the same account remain possible. Bereavement and trust administration has been described across multiple reviews in terms that suggest significant distress.

Several reviewers explicitly state they were forced to chase twenty or more times before their issue was resolved. The pattern here is not occasional poor service. It is a process infrastructure that is visibly struggling.

2. The fee restructure backlash

As covered above, the March 2026 changes were framed as a reduction and experienced by many customers as an increase. The ISA fee cap comparison comes up repeatedly, with customers citing AJ Bell’s £42 cap against HL’s new £150 directly. Interactive Investor is also cited as a cheaper alternative across multiple reviews. Customers are doing their own research and drawing their own conclusions.

3. Platform and app failures

Two distinct issues have emerged here.

The first is a structural gap HL has confirmed has no fix timeline: the Cash ISA cannot be transacted through the app at all. It can only be viewed. Any instruction requires logging in via the website. In 2026, for a platform managing over £172 billion, that is a meaningful limitation.

The second is a data feed failure running for several months at the time of writing. Price charts are broken across holdings. Dividend history is missing. Market data is delayed or incorrect. One reviewer noted they now use competitor websites simply to research their own HL holdings.

A fourth theme worth naming

Across dozens of reviews, customers with relationships spanning ten, fifteen and thirty five years describe a sharp deterioration in service quality since the March 2025 takeover. The specific observations that recur are: staff redundancies, a call centre feel that did not previously exist, responses that read as AI generated rather than personal, and no named complaint owners.

These are not the reviews of people who had one bad experience. They are the reviews of people who had a long, positive relationship with a platform and are watching something change in real time.

Where HL Genuinely Wins

This review has covered significant difficult material. So let me be equally specific about what HL does genuinely well.

Phone based customer support is HL’s clearest and most consistent strength. Even in the most negative Trustpilot reviews, a pattern repeats itself: the people on the phone are praised. Helpful, knowledgeable, patient with less experienced investors, able to walk someone through an unfamiliar process without making them feel foolish. The complaints are almost entirely directed at the systems behind the human contact, not the humans themselves.

HL operates a Bristol based helpdesk available Monday to Friday plus Saturday mornings. For a woman managing a SIPP or ISA for the first time, that accessibility has genuine, tangible value that a fee table alone does not capture.

Breadth of investment choice is strong, with over 13,000 options including shares, funds, ETFs, investment trusts, bonds and gilts.

Research tools and educational resources are deep and well regarded, integrated throughout the platform and easy to find. For a newer investor who wants context alongside the ability to make her own decisions, this is a meaningful differentiator.

The Junior ISA stands apart. Every holding is held completely free of charge and online dealing is also free across all asset types. It is the only account where HL charges nothing at platform level, and one of the strongest Junior ISA offerings from any major UK platform.

Ready made portfolios are available for investors not yet ready to choose their own funds, starting from as little as £25 per month or a £100 lump sum.

Hargreaves Lansdown vs Interactive Investor: A Direct Comparison

I chose Interactive Investor seven years ago and I would make the same choice again today. But rather than just tell you that, here is the direct comparison so you can make your own call.

| Hargreaves Lansdown | Interactive Investor | |

|---|---|---|

| Fee structure | Percentage based: 0.35% up to £250k | Flat monthly fee: £5.99 (Core) or £14.99 (Plus) |

| Annual cost at £50k | £175.00 | £71.88 (Core) / £179.88 (Plus) |

| Annual cost at £77k | £269.50 | £179.88 (Plus) |

| Annual cost at £100k | £350.00 | £179.88 (Plus) |

| Stocks and Shares ISA | 0.35%, capped at £150/yr | Included in flat fee |

| SIPP | 0.35%, capped at £12.50/month | Included in flat fee |

| Junior ISA | Free, all asset types | Included in flat fee |

| Fund trades | £1.95 per trade | £1.49 per trade |

| Share trades | £6.95 per trade | £3.99 per trade (one free credit/month on Plus) |

| Regular investing | Free via Direct Debit | Free via Direct Debit |

| Phone support | Bristol helpdesk, Mon to Fri plus Saturday mornings | Limited phone access |

| Account types | 8 account types | 4 account types |

| Investment options | 13,000+ | 40,000+ |

| App experience | Cash ISA app-only viewable; data feed issues ongoing | Functional; I deleted it to stop over-monitoring |

| Pension transfers | Currently 8 to 12 weeks, limited communication | 2 to 3 weeks, regular updates |

| Trustpilot score (Jun 2026) | 4.3 | 4.6 |

| Ownership | Private equity (CVC, Nordic Capital, ADIA) since March 2025 | Owned by abrdn |

| Regulation | FCA regulated, FSCS protected to £85k | FCA regulated, FSCS protected to £85k |

Is Hargreaves Lansdown Right for Women Planning Retirement?

Here is the honest breakdown.

If you are just starting out and your portfolio is still relatively small, HL’s phone based support is a genuine consideration in its favour. Being able to call a knowledgeable, patient human being when something feels confusing has real value that a fee comparison table does not fully capture. At portfolio sizes under £50,000, the fee difference versus a flat fee platform is small enough that the comfort of HL’s helpdesk accessibility may well be worth it.

If you are building both an ISA and a SIPP simultaneously, this is the profile that needs to think most carefully. A woman in her forties or fifties holding both accounts is running two percentage fee accounts simultaneously. Every year both portfolios grow, HL charges more on both. The fee gap versus a flat fee platform does not just persist. It widens every single year.

At £77,000 combined across ISA and SIPP, you are already paying £89.62 more per year with HL than with Interactive Investor. At £150,000 combined that gap becomes £345.12 per year. At £200,000 it becomes £520.12. That is money that could be compounding for your retirement instead of paying platform fees. For the woman who started later and is now working hard to close the gap, every pound of unnecessary cost matters more.

On the Junior ISA specifically, HL has a clear and unambiguous advantage for parents investing alongside their own retirement planning. If a Junior ISA is your primary or only account, HL’s free structure wins outright.

On timing: HL is in the middle of a significant transition. The private equity owners have signalled ongoing technology investment and platform transformation. That transformation may ultimately produce a better, more competitive platform. It may not. Either way, the customer experience data suggests the transition period is uncomfortable for existing customers right now.

Starting a long term financial relationship with a platform that is mid transformation, with fees that recently moved against the type of investor you are, and with operational performance currently under strain, is not the same decision it would have been two years ago.

Verdict

Hargreaves Lansdown is not a bad platform. Before December 2025 it was arguably the most trusted retail investment platform in the UK, and that reputation was earned over four decades of genuinely good service.

But this review is being written in June 2026, and the platform you would be joining today is not the one those long-standing customers fell in love with. The fee restructure landed framed as a reduction and was experienced by many as an increase. The Trustpilot score dropped 0.71 points in a few months and has not recovered. Operational complaints are running at a scale that suggests systemic strain rather than isolated incidents. Customers with thirty-five year relationships are leaving.

Would I choose it today? No. And not primarily because of the fees, though the fee gap compounds significantly over time.

I would not choose it because of the transfer experience. Consolidating old pension pots is the moment a platform first proves whether it deserves your trust with something that genuinely matters. Right now, the evidence suggests HL is making that process harder and more stressful than it needs to be. When I transferred my own pensions into Interactive Investor, it took two to three weeks with regular updates at every stage. That experience built trust that has kept me there for seven years.

Who should still consider HL: if you are early in your investing journey and know you will want to speak to a knowledgeable human regularly, HL’s helpdesk remains a genuine differentiator. For a Junior ISA specifically, its completely free structure is outstanding.

If HL completes its transformation and satisfaction data returns to pre-2025 levels, I will update this post.

The bottom line: a credible, FCA-regulated platform with real strengths, currently in visible transition, with fees that have moved against long-term investors and operational performance not yet matching its brand reputation. Do your own maths and make the decision that is right for your situation.

I am currently in the process of joining the Hargreaves Lansdown affiliate programme. In the meantime you can visit Hargreaves Lansdown directly at hl.co.uk.

FAQ

1. What is Hargreaves Lansdown and who is it best suited for? Hargreaves Lansdown is the UK’s largest investment platform, offering ISAs, SIPPs, ready-made portfolios, and savings products in one place. It is best suited to long-term investors who value research tools, customer support, and a wide investment range over the lowest possible costs. Active traders and cost-conscious investors tend to find better value elsewhere.

2. How much does Hargreaves Lansdown charge? Following a major fee overhaul in March 2026 (its first in over 10 years), Hargreaves Lansdown charges 0.35% per year on Stocks and Shares ISA and SIPP accounts, capped at £150 per year for shares, ETFs, investment trusts, and bonds. Fund dealing starts from £1.95, and share dealing is capped at £6.95 per online trade.

3. Is Hargreaves Lansdown good for ISAs? Yes. It offers a Stocks and Shares ISA, a Cash ISA, a Lifetime ISA, and a Junior ISA. The Junior ISA has no service fees or trading charges, making it a popular choice for parents saving for children.

4. Can I open a SIPP with Hargreaves Lansdown? Yes. Hargreaves Lansdown is one of the UK’s most popular SIPP providers, with access to over 13,000 investments. The annual charge is 0.35% (capped at £150 per year for shares and ETFs), making it competitive for smaller pension pots but potentially expensive for larger ones.

5. What do customers say about Hargreaves Lansdown? HL scores 4.3 overall but the monthly data tells a more nuanced story. Between July and November 2025 scores consistently ran between 4.58 and 4.69. Following the December 2025 fee announcement scores dropped sharply, hitting a low of 3.75 in February 2026 with one star reviews reaching 23% that month. The platform is recovering but has not returned to pre-announcement levels.

6. What are the main drawbacks of Hargreaves Lansdown? The main criticism is cost. While the 2026 fee cuts have helped some, it remains one of the pricier UK platforms.

Sources:

- Hargreaves Lansdown Review 2026 (Money to the Masses)

- Hargreaves Lansdown Review 2026 (StockBrokers.com)

- Hargreaves Lansdown Pros and Cons (Unbiased)

- Hargreaves Lansdown Charges (HL.co.uk)

- Hargreaves Lansdown SIPP Charges Explained (BrokerChooser)

- Trustpilot Reviews

Angelina is the founder of Investing Adventures, where she helps women build confidence with money and investing. With seven years of personal investing experience, she breaks down complex financial topics into practical, actionable advice. Her mission is simple: to help more women take the driver’s seat in their financial future.

I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.