I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.

There’s a particular kind of putting off that doesn’t feel dramatic at all. It sits quietly underneath the to do list, insisting that everyone else already knows how to do this investing thing and that the moment to start was years ago. Let me gently tell you it isn’t too late. It only feels that way.

Most investing guides read as though they were written for someone in their twenties: no mortgage, no children, a spreadsheet already open and ready to go. None of them read like they were written for a woman in her forties, fifties or sixties, because they weren’t.

I’m Angelina, I’m 52 at time of writing. Seven years ago I knew nothing about investing. Not a clue. I picked up a book because I liked the cover (turns out The Wealth Chef isn’t actually about cooking, who knew), no financial background, no qualifications, nothing beyond curiosity and a growing sense that I needed to sort my money out before it sorted itself out for me. These days I manage five accounts, a SIPP, a self invested ISA, a Trading Account, and two Junior Self invested ISAs for my kids, built from seven years of real decisions with real money.

I’m not a financial advisor. I’m not an expert. I’m a woman who figured this out later than she’d have liked, made a few wrong calls along the way, and came out the other side actually knowing what she’s doing. This guide sets out exactly how to start investing in the UK, step by step, starting from wherever that journey begins.

Table of Contents

The Jaw Drop Moment

Here’s a number that stopped me in my tracks the first time I saw it.

Put £200 a month into a savings account earning 3% interest, and leave it for twenty years. It grows to £65,660. £48,000 paid in, £17,660 earned in interest on top. Solid. Safe. Unremarkable.

Put that same £200 a month into a stocks and shares investment averaging 7% a year, over the same twenty years, and it grows to £104,185. Same £48,000 paid in. This time growth adds £56,185, more than three times what the savings account earned.

| Savings account (3%) | Invested (7% average) | |

| Monthly contribution | £200 | £200 |

| Paid in over 20 years | £48,000 | £48,000 |

| Total after 20 years | £65,660 | £104,185 |

| Growth earned | £17,660 | £56,185 |

Same discipline. Same £200 a month. Same twenty years. The only thing that changed is where the money sat. That difference, £38,525, is what “safe” actually costs.

A word of honesty here. 7% is a long term average, not a promise for any single year. Some years will be up double digits, some years will be down, and there will be periods that feel genuinely uncomfortable to sit through (I’ll come back to that later). But historically, over meaningful stretches of time, this is roughly the size of the gap between money that sits in cash and money that gets put to work.

First Things First: What Investing For Beginners UK Actually Means Before You Start

Before any of the numbers above mean anything, there are two boxes to tick. Skip them and investing stops being clever and starts being reckless.

An emergency fund, sitting in cash, covering three to six months of essential expenses.

This is the fund that exists purely so a boiler breaking down or a job loss doesn’t force a sale of investments at exactly the wrong moment. Investments need time to do their work uninterrupted, that’s the whole thesis behind the jaw drop numbers above, so if there’s a real chance that money will be needed within the next few years, it shouldn’t be invested at all. It belongs in an easy access savings account, boring and available, doing its actual job.

High interest debt, cleared first.

Credit cards, store cards, anything charging 15%, 20%, 25% or more, need to be paid off before a single pound goes into an investment account. No investment reliably returns more than the interest that debt is costing. Clearing a 22% credit card is, in effect, a guaranteed 22% return. Nothing further down this guide beats that.

I know how tempting it is to skip straight to the interesting bit. I wanted to invest the day I understood how those numbers worked. But the order matters. Emergency fund first, expensive debt cleared second, then investing. Once both boxes are genuinely ticked, everything from here is about putting money to work properly instead of leaving it exposed.

Once both boxes are ticked, there’s a shift worth making before opening any account. I pay a fixed amount into my SIPP the moment I’m paid, and live on what’s left. Not the other way around, waiting to see what’s spare at the end of the month. That single change, paying my future self first instead of last, made more difference than any account or fund choice I made afterwards.

What’s Actually Happening When You Invest

Strip away the jargon and investing comes down to something remarkably simple: buying a small piece of something that has a genuine chance of being worth more later.

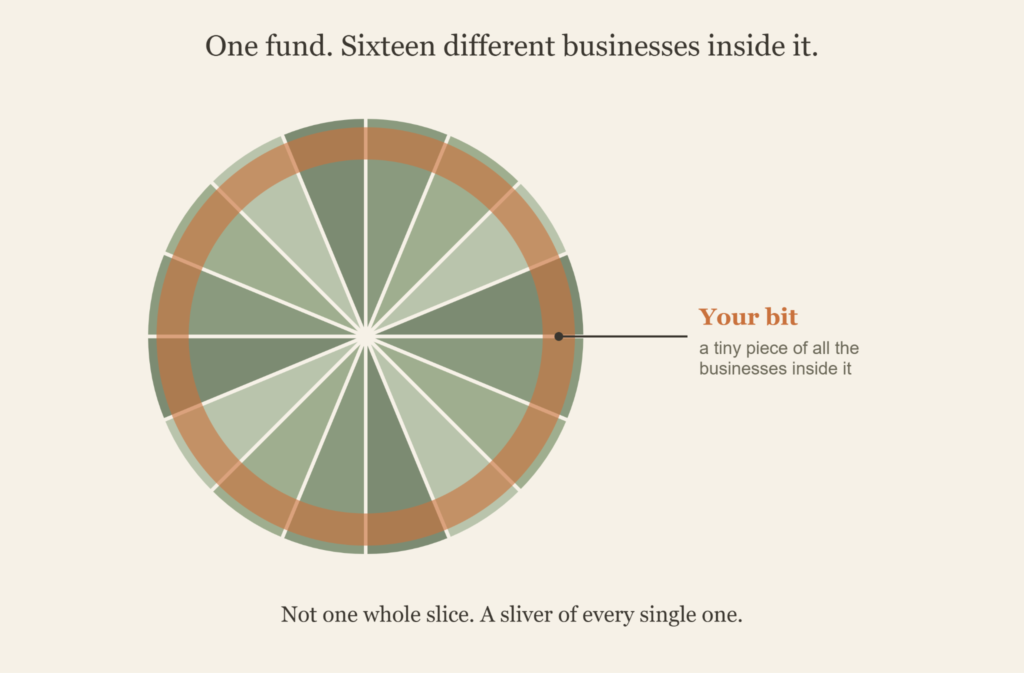

That something might be one company, in which case it’s called a share, literally a share of that business. Own a share in a company and there’s ownership of a tiny sliver of it: its buildings, its stock, its future profits. More commonly, especially when starting out, that something is a collection of hundreds or thousands of companies bundled together into a single fund, so instead of betting on one business doing well, the bet is on a whole slice of the economy doing well over time (more on how that works later).

Either way, the mechanism is the same. Money buys ownership. Ownership grows, or shrinks, in line with how those businesses actually perform. Over meaningful stretches of time, businesses tend to grow: they sell more, earn more, and become worth more. That growth is where investment returns come from. It isn’t magic and it isn’t a trick. It’s ownership, doing what ownership does.

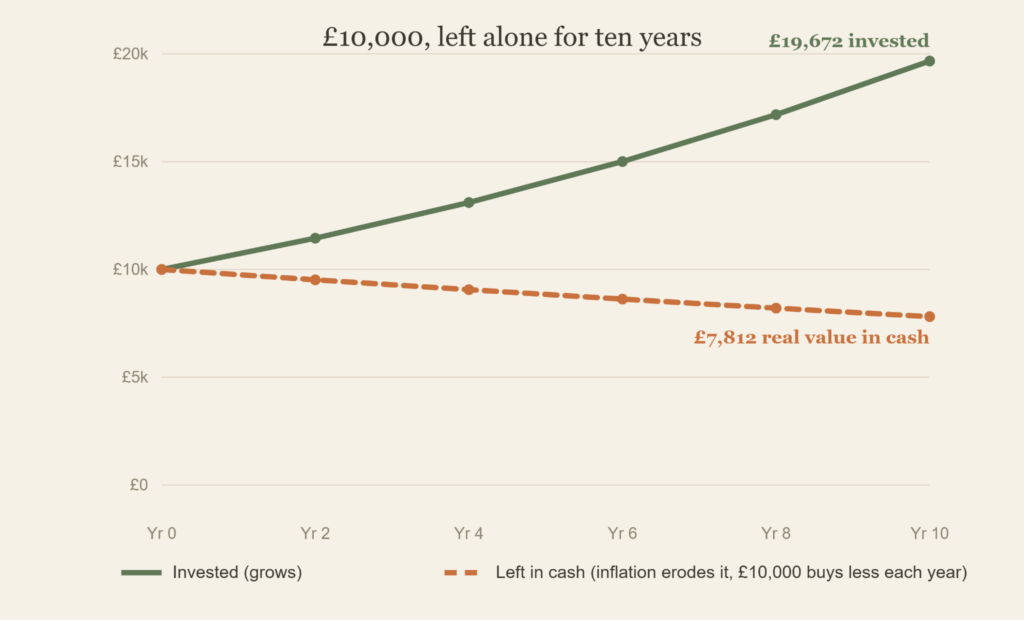

Saving is a different mechanism entirely. Money sitting in a savings account doesn’t own anything. It just sits, waiting, occasionally earning a small amount of interest for the privilege of sitting there. And while it sits, inflation is quietly doing its own work in the background, eroding what that money can actually buy. £10,000 sitting still for ten years doesn’t stay worth £10,000. It just looks like it does, right up until it’s time to spend it.

That’s the real difference. Saving preserves the number. Investing aims to grow the value. Both have a place, the emergency fund from the last section absolutely belongs in cash, but conflating the two, treating a savings account like it’s doing the job of an investment, is one of the quiet reasons so many of us reach our fifties feeling like there should be more to show for decades of careful saving.

The Accounts You Need To Know About

There are three accounts that come up again and again in UK investing, and getting familiar with what each one actually does removes most of the confusion before it starts. None of them are investments in themselves. They’re wrappers, containers that hold whatever’s invested inside them and determine how tax works on the way in, and on the way out.

Stocks and Shares ISA

A Stocks and Shares ISA is a tax wrapper that shelters investments from capital gains tax and dividend tax entirely. Load it with cash, buy a fund inside it, watch it grow, and none of that growth is taxed, not now, not when it’s eventually withdrawn.

The annual allowance is £20,000 (correct at the time of writing, always worth checking the current figure), and that allowance resets every tax year. It doesn’t roll over, so unused allowance is simply gone once April rolls round again.

It suits pretty much everyone wondering how to start investing in the UK, because unlike a pension, the money isn’t locked away. It stays accessible, which makes it the natural first account for medium term goals sitting somewhere between an emergency fund and a full retirement pot.

There’s a full breakdown of how mine actually works day to day, including the real fee structure and real numbers, in my Interactive Investor review.

SIPP

A SIPP, a Self Invested Personal Pension, is the account built specifically for retirement. The mechanic worth understanding properly is tax relief. Contribute into a SIPP and the government adds 20% on top automatically, as basic rate tax relief, no paperwork required. It simply lands in the account a few weeks later. Higher rate taxpayers can claim further relief through self assessment, but that basic 20% arrives regardless.

The thing that scared me most when I opened mine was the locked nature of it. Money inside a SIPP can’t be touched until 57 under current rules. That felt like a wall in the beginning. It isn’t. It’s the entire point.

My own turning point came when I stopped fighting that and accepted what a SIPP is actually for: a locked box for future me. I’d been keeping spare money in my ISA instead, telling myself it was for the long term, and then quietly dipping into it because it was there and it was accessible. It never had a real chance to grow. The moment that excess money moved into the SIPP instead, and stayed untouchable, the growth became something else entirely.

Full detail on how the SIPP has performed over seven years, including the tax relief timeline and consolidating old pensions into it, is in my Interactive Investor review.

Junior ISA

A brief one, because the mechanics are simple. A Junior ISA is the same tax free wrapper as an adult ISA, opened on behalf of a child, with an annual allowance of £9,000 (correct at the time of writing). The money belongs to the child and becomes fully theirs at 18.

Mine came about through a gift. My father gave money to my two children and asked me to put it somewhere sensible. I invested it in the same index tracker funds already working well inside my own SIPP. Investing gifted money that wasn’t mine, and watching the value move, was frightening in a way my own investments never were. But the logic held. There was conviction in those funds for my own retirement, so there was no reason to apply different logic to theirs.

More on how that decision has played out is in my Interactive Investor review.

What To Actually Invest In As A Beginner

Once the accounts are sorted, the actual question is what goes inside them. For almost everyone starting out, the honest answer is an index fund. But that phrase hides two different things worth untangling first: an index, and an index tracker fund.

An index is simply a list, a scorecard that measures how a particular group of companies is performing. The FTSE 100 tracks the 100 biggest companies listed in the UK. The S&P 500 tracks the 500 biggest companies in the US. The MSCI World index tracks thousands of companies across dozens of countries.

An index tracker fund is the product that makes an index investable. It’s a single fund built to hold the same companies as its chosen index, in roughly the same proportions, so its value moves in line with that index. Buy one slice of a tracker fund, and the outcome mirrors the FTSE 100, or the S&P 500, or the world, depending which tracker was chosen.

The alternative to a tracker is betting on one company (buying a share in a single business), or paying someone else, an active fund manager, to pick a selection of companies instead. Both are really the same wager: that a person, whether an individual investor or a professional, can consistently spot the winning companies ahead of everyone else, year after year.

Most active fund managers don’t. Studied over meaningful stretches of time, most fail to beat the very index they’re trying to outperform, once fees are taken into account. And those fees matter more than they sound like they should. An active fund charging 1% a year against a tracker charging 0.15% sounds like a rounding error. Over twenty years, on a growing portfolio, that gap alone can quietly cost tens of thousands of pounds, money that never had the chance to compound because it was paid out in fees instead.

The logic underneath all of this is simple. Betting on one company means backing a single business to get everything right, indefinitely. Buying a slice of the whole market, through a tracker fund, means the outcome depends on the economy broadly moving forward over time, which it has, reliably, for as long as there’s data to check. Some companies inside that index will fail. Some will thrive. The index absorbs both and, historically, keeps climbing regardless.

How Much Money It Actually Takes To Start Investing

Less than you’d think. The platform I invest with (Interactive Investor) lets you start regular investing from as little as £25 a month, and most other platforms are the same. There’s no minimum lump sum required, no need to wait until a spare £5,000 or £10,000 turns up somewhere.

That waiting is actually the expensive part. Starting small and consistent now, today, the moment it’s possible, beats waiting for a bigger sum to arrive, because time invested matters more than the size of any single contribution. £25 a month started today has years longer to grow than £250 a month started in five years’ time.

Investing a fixed amount on a set schedule, rather than as one lump sum, has a name: pound cost averaging. Buying another slice of the same fund every month means sometimes buying when prices are high and sometimes when they’re low, which averages out the price actually paid over time and smooths out the effect of short term ups and downs. It won’t guarantee the best possible price in any given month. What it does is remove the pressure of trying to pick the perfect moment, which nobody, professional or otherwise (including me), can reliably do anyway.

Start with whatever’s available. £25, £50, £100. The amount matters far less than simply beginning.

Choosing A Platform

Once the account type and the fund are settled, the last decision is which platform actually holds it all. A few things are worth checking before signing up anywhere.

FCA regulation. Any UK platform should be authorised and regulated by the Financial Conduct Authority, with investments protected by the Financial Services Compensation Scheme up to £85,000. This isn’t optional. Skip it and there’s no protection at all if something goes wrong.

Account types available. Not every platform offers every account. Some cover ISAs and SIPPs well but skip Junior ISAs entirely, or vice versa. Check the platform actually offers everything needed, now and for whatever comes next.

Fee structure. Platforms charge either a flat monthly fee or a percentage of the portfolio, and which one works out cheaper depends entirely on the size and number of accounts held. Worth doing the actual maths rather than assuming, because the gap between the two models widens every year a portfolio grows.

Ease of use. A platform that feels confusing gets checked less, understood less, and trusted less. That matters more than it sounds like it should, particularly when starting out.

I have written detailed reviews of two of the most popular platforms for UK women investors. Read my Interactive Investor review and my Hargreaves Lansdown review to understand which might suit your situation.

Mistakes Beginners Actually Make (Because I’ve Made Them)

None of what follows is theoretical. I made every one of these mistakes myself, in the first couple of years, before I properly learned to leave the whole thing alone.

Checking the app too often.

In the early days I had the app on my phone, and I checked it constantly. Every small movement got noticed. Every dip felt personal. That habit wasn’t harmless. It fed straight into the next mistake.

Reacting emotionally to dips.

Watching a portfolio move, even by a small amount, triggers something that has nothing to do with sound strategy. A dip that means nothing over twenty years can feel like a crisis in the moment I was actually watching it. I reacted to those moments more than once, and every single time it made things worse, not better.

Over trading.

Constant checking and emotional reacting led me to buy and sell far more than I should have. Every one of those extra trades was an attempt to fix a feeling, not a genuine investment decision, and the effect on growth was genuinely detrimental. The fix, in the end, was deleting the app entirely. I now check my accounts once every two months, on desktop, on purpose. The difference in growth since that one change has been significant.

Treating the ISA like a savings account.

This one is subtler, and it went on for years. My ISA sat there looking exactly like a savings account, easily accessible, always visible, and I used it exactly like one. Dipping in whenever something came up. That money never had the chance to actually grow, because I never really left it alone long enough to.

The lesson underneath all four of these is the same one, said differently each time. Investing works when it’s left uninterrupted. Every mistake on this list came down to me interrupting it

Your First Five Steps

Here’s exactly what to do, in order.

- Decide how much can be invested each month without missing it. Not a number that feels aspirational. A number that could disappear from a bank account and genuinely not be noticed a week later.

- Open a Stocks and Shares ISA on an FCA regulated platform. Check the regulation, check the fees, then get it open. This is the account, not the investment itself.

- Choose a low cost global index fund. One fund, spread across thousands of companies, charging a fraction of a percent. That’s the whole strategy at this stage.

- Set up a monthly direct debit so it happens automatically. The same amount, the same date, every month, without a decision required each time.

- Delete the app and check the portfolio no more than once every two months. This is the step that protects everything above it.

Five steps. None of them complicated. All five, done in order, is genuinely more than most people manage in a lifetime of meaning to get round to it.

Frequently Asked Questions

What should I invest in as a beginner in the UK?

For most beginners, a low cost global index tracker fund, held inside a Stocks and Shares ISA, is the simplest and most sensible starting point. It spreads money across thousands of companies rather than betting on one, keeps fees low, and doesn’t require picking winners. Once an emergency fund is in place and any high interest debt is cleared, opening an ISA, choosing one global tracker, and setting up a monthly direct debit is genuinely enough to begin.

Is £1,000 enough to invest?

Yes, easily. A thousand pounds can be invested as a lump sum, or drip fed into an account over several months. There’s no minimum portfolio size that makes investing worth it. What matters far more than the amount is getting money into a low cost index fund, inside a tax wrapper like an ISA, and leaving it alone to grow for years rather than months. Time in the market matters more than the size of the starting sum.

Can I start investing with £100?

Yes. Most UK platforms accept lump sums and monthly contributions well below a hundred pounds, some from as little as £25 a month. A hundred pounds invested in a low cost index fund and left alone for years will genuinely compound, exactly the same mechanism that applies to larger sums. The habit of investing regularly matters more at this stage than the size of any single contribution, so starting today beats waiting for a bigger amount later.

How long should you invest for in the UK

As a general rule, only invest money you will not need for at least five years, ideally longer. Markets go up and down in the short term, but historically they reward patience over time. Saving for something in the next year or two? A Stocks and Shares ISA is not the right home for that money, a Cash ISA is. Investing is not a get rich quick scheme. It is a get rich slowly, boringly, consistently scheme, and I have lived that with my own SIPP and ISA for seven years.

Do I need a financial adviser to start investing?

Not necessarily. Self directed platforms like Interactive Investor are built for exactly this, choosing a fund and managing an account without a middleman. A financial adviser becomes genuinely worth the cost with larger, more complex situations, inheritances, multiple pensions, or six figure sums. For most beginners starting with a monthly contribution into a single index fund, a well chosen platform and a bit of research is enough to get moving safely.

Angelina is the founder of Investing Adventures, where she helps women build confidence with money and investing. With seven years of personal investing experience, she breaks down complex financial topics into practical, actionable advice. Her mission is simple: to help more women take the driver’s seat in their financial future.

I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.