I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.

You’ve typed it into Google. Probably more than once, probably late at night, probably closing the tab before you got to the end of whatever came back. How much do I need to retire in the UK?

And every answer you found did one of two things. It either gave you a number so enormous it felt hopeless, a million pounds, more, built for someone who started saving at 25 and never stopped. Or it handed you a formula so tangled in assumptions and percentages that interpreting it felt like a job in itself. Neither answer was written for you. Almost none of them were written for a real woman with a real life, career breaks, part time years, children, a pension she only half remembers opening.

Here’s the thing most of those guides quietly get wrong, and it changes everything: they forget the state pension. They calculate the pot you’d need as though your private savings have to do all the work alone, and the number comes out hundreds of thousands of pounds bigger and more frightening than it needs to be. We’re going to do the honest maths instead.

I’m Angelina, I’m 52, and I’ve been investing for seven years. I built a SIPP from scratch after digging three forgotten pensions out of old paperwork and consolidating them into one place. I have asked this exact question myself, sat with the scary numbers, and worked out what they actually mean for someone in my position. This guide gives you a real answer, for a real woman, with real numbers you can check for yourself.

Let’s get into it.

Table of Contents

The honest answer first.

I’m not going to bury it.

The commonly cited rule is that you’ll want around 70% of your pre retirement income each year once you stop working. And the rule of 25 says that to work out your target pot, you multiply your desired annual retirement income by 25. So a woman wanting £25,000 a year in retirement needs roughly £625,000 across all her sources, and crucially, that includes the state pension.

Now let me immediately soften that number, because on its own it’s misleading. It is not fixed, and it is almost certainly not what your private pension alone needs to provide. Your real number depends on when you want to retire, what the state pension contributes, whether you own your home, what you’ll actually spend, and how long you plan to draw on the pot. The rest of this guide unpacks each of those, one at a time, and by the end you’ll have calculated your own number rather than borrowing someone else’s.

The state pension: what it actually gives you.

Most guides skip past this or mention it as a footnote. It should not be a footnote. It should be the first line of your calculation.

The full new state pension is currently £241.30 a week, which works out at £12,590.69 a year (correct at the time of writing, and it changes each April, so always check the current figure). To get the full amount you generally need 35 qualifying years of National Insurance contributions.

Sit with what that means for a moment. £12,590 a year, for life, inflation protected, before your private savings contribute a single pound. Using the rule of 25, providing that income yourself would take a pot of over £300,000. The state pension hands you that, which means every calculation that ignores it, and plenty of the big pension industry articles do exactly that, overstates what you need to save by hundreds of thousands of pounds over a retirement.

So here is the single most useful five minutes you’ll spend on your retirement this year. Go to gov.uk/check-state-pension and get your personal forecast. Right now, before you read on if you like. It will tell you exactly what you’re on track to receive and from what age.

This matters especially for women. Career breaks, part time years, time spent raising children, all of these can leave gaps in your NI record, and many of us have them without knowing. The forecast shows you any gaps, and in many cases you can fill them by making voluntary contributions, which is often one of the best value retirement moves available. Check first, then decide.

How much income do you actually need?

Before any pot size means anything, you need a realistic picture of what retirement actually costs. The most useful framework here comes from the Retirement Living Standards, produced by Pensions UK with Loughborough University, which describe three levels of retirement lifestyle and what each costs per year for a single person outside London:

| Living standard | Annual income, single person | What it looks like |

|---|---|---|

| Minimum | £13,900 | Essentials covered, no car, a week’s holiday in the UK |

| Moderate | £32,700 | More financial security and flexibility, a foreign holiday, running a car |

| Comfortable | £45,400 | More financial freedom, longer trips, more generosity with family |

Two things worth noticing. First, the Minimum standard is only about £1,300 more than the full state pension alone. Second, and this is the honesty these figures don’t shout loudly enough about: they assume you own your home outright. No rent, no mortgage. They also exclude social care costs entirely, which is one of the largest financial risks of later life. If you’ll be renting in retirement, or you want to plan seriously for the possibility of care, your real number sits meaningfully above these headline figures. Useful anchors, not a personal budget.

What is a good pension pot at different ages.

The honest answer to “what is a good pension pot” is: one that closes the gap between the income you want and the income the state pension gives you, by the age you want to stop working. That gap logic is what drives every figure below, and I’ll show you the full calculation in a moment. First, the ages everyone actually asks about.

What is a good pension pot at 65?

If you’re retiring close to state pension age, your pot only has to fund the gap. For a woman wanting a moderate £28,000 a year, the gap after the £12,590 state pension is £15,410, which the rule of 25 turns into a target pot of roughly £385,000. Want a Minimum standard lifestyle instead? The gap is barely £1,300 a year, and the pot needed shrinks to around £33,000. The income you choose changes everything, which is exactly why a single universal number is useless.

What is a good pension pot at 60?

Retire at 60 and there’s a stretch of years before the state pension arrives, and your pot has to carry the whole load on its own through them. Bridging seven years at £28,000 a year adds roughly £196,000 on top of the £385,000 above, so a realistic target for that lifestyle is somewhere around £580,000. That’s the real cost of retiring early: not a bigger lifestyle, just more years funded entirely by you.

What is a good pension pot at 55?

The same logic again, stretched further. Bridging twelve years at £28,000 adds around £336,000, taking the target to roughly £720,000. One practical note here: money in a pension can’t usually be touched until the minimum pension age of 55, rising to 57 from 2028, so anyone planning a very early retirement needs accessible savings, an ISA for instance, to cover the years before the pension unlocks. My How To Start Investing guide covers how those wrappers fit together.

These are planning anchors built on the rule of 25 and today’s state pension, not guarantees, and the rule of 25 itself has limits I’ll come back to. But they’re honest anchors, which is more than most of the numbers you’ll have seen.

Average retirement savings by age UK: are you behind?

Now for the question underneath the question. You don’t just want to know the target. You want to know whether you’re behind everyone else.

So here is what the actual UK data says, and it is nothing like what pension industry marketing implies. According to the Office for National Statistics, the median private pension wealth among UK adults who have pension savings is £57,500. Across all adults, including those with nothing saved, it drops to £19,700. And according to the Financial Conduct Authority, the average pot for people actually accessing their pensions at 55 and over is around £107,300.

Read those again. The average woman reaching pension access age has around £107,000, not £625,000, not a million. Most people are starting from much further back than the industry pretends, and I think saying that plainly matters (and honestly that made me feel so much better when I did the research around this). If your pot is £20,000, £40,000, £60,000 right now, you are not uniquely behind. You are roughly where the median of the country is, being sold targets calibrated for the top few percent.

That’s the context. Here’s what on track actually looks like, derived from the same £385,000 at 67 target using the gap method above, assuming 7% average annual growth (a long term historical average, never a promise):

| Age | Roughly on track for £385,000 at 67 |

|---|---|

| 40 | £62,000 already invested, if you stopped adding today |

| 50 | £122,000 already invested, if you stopped adding today |

| 60 | £240,000 already invested, if you stopped adding today |

Those figures assume no further contributions, which is why they look demanding. Keep contributing monthly, as almost everyone does, and the amount you need already banked at each age falls considerably. Which brings us to the calculation that actually matters: yours.

How to calculate your own retirement number.

Three inputs. Three steps. A calculator on your phone is all you need.

Your inputs:

- The annual income you want in retirement. Use the Retirement Living Standards above as a starting point and adjust for your own housing situation.

- Your state pension entitlement. From your gov.uk forecast, not a guess.

- The number of years until you retire.

Your steps:

- Subtract your annual state pension from your annual desired income. That’s your gap, the part your own savings must provide.

- Multiply the gap by 25. That’s your target pot.

- Work backwards to a monthly contribution. How much, invested each month between now and retirement, gets you there.

A worked example. Take a woman aged 52, wanting £28,000 a year in retirement at 67, with a full state pension entitlement of £12,590.

Her gap is £28,000 minus £12,590, which is £15,410 a year. Her target pot is £15,410 times 25, roughly £385,000. Notice how different that is from the £700,000 that the same £28,000 income implies if you ignore the state pension, which is precisely what many big provider articles do. Including it nearly halves the mountain.

With 15 years to build it, starting from scratch, and assuming 7% average annual growth, she needs to invest roughly £1,200 a month. And before that number makes you close the tab, hold on, because tax relief is about to shrink it, and the next section shows you exactly how.

Not everyone can do £1,200 a month, so find yourself in these numbers instead. Same woman, same 15 years, same 7% assumption:

| Monthly investment | Pot at 67, roughly | Annual income with state pension, roughly |

|---|---|---|

| £500 | £158,000 | £18,900 |

| £800 | £254,000 | £22,700 |

| £1,000 | £317,000 | £25,300 |

| £1,200 | £380,000 | £27,800 |

Every row on that table is a real retirement. None of them is failure. The point of the calculation is not to shame you toward the biggest number, it’s to let you choose your trade offs with your eyes open.

What if you are starting late.

This is the section you actually came for, and the one no generic guide writes properly. So let me address it directly.

Starting at 52 is not the same as starting at 32. I won’t pretend otherwise, compounding rewards time above everything else. But it is nowhere near hopeless, and the levers available to you are more powerful than you think.

The state pension is your foundation. As we’ve seen, it quietly provides what a £300,000+ pot would otherwise have to, and filling any NI gaps strengthens it further.

Adjusting the income target helps. The gap between a £28,000 retirement and a £24,000 retirement is a £100,000 difference in the pot required. Moving the target is not defeat, it’s arithmetic.

Downsizing helps. For homeowners, the house is often the largest asset on the sheet, and releasing some of its value later in the plan changes the numbers considerably.

Working slightly longer helps more than almost anything. Two extra years means two more years of contributions, two more years of growth, and two fewer years of drawdown, all pulling in the same direction at once. The effect on the final pot is significant.

And here’s my own experience, because it belongs in this section. I started later than I would have liked, at 45, with three forgotten pensions and no financial background. I made real mistakes in the early years, checking my investment app constantly, reacting emotionally to every dip, trading far more than I should have. The turning point was stopping all of that: deleting the app, contributing consistently every single month, and leaving the whole thing alone. The growth since then has been extraordinary. Not because I found a clever fund or timed anything well, but because I finally let compounding do its job uninterrupted. I’ve written honestly about all of it, mistakes included, in my Interactive Investor Review.

If you’re starting today at 50 or 55, you’re not too late. You’re just on a plan with less slack in it, which makes starting this month, rather than next year, matter more, not less.

The SIPP: why it matters for closing the gap.

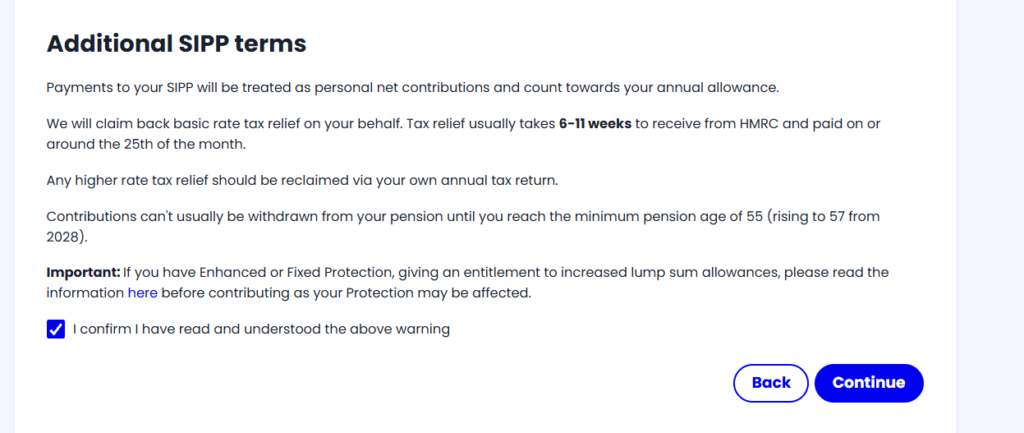

If you’re playing catch up, one tool matters more than any other, and that’s the tax relief on a SIPP.

Here’s the mechanic in plain terms. Contribute into a SIPP as a basic rate taxpayer and the government adds 20% on top of the gross amount automatically. In practice that means every £100 that lands in your pension only costs you £80, a 25% uplift on every pound you put in, with no paperwork required (phew). Higher rate taxpayers can claim further relief through self assessment on top.

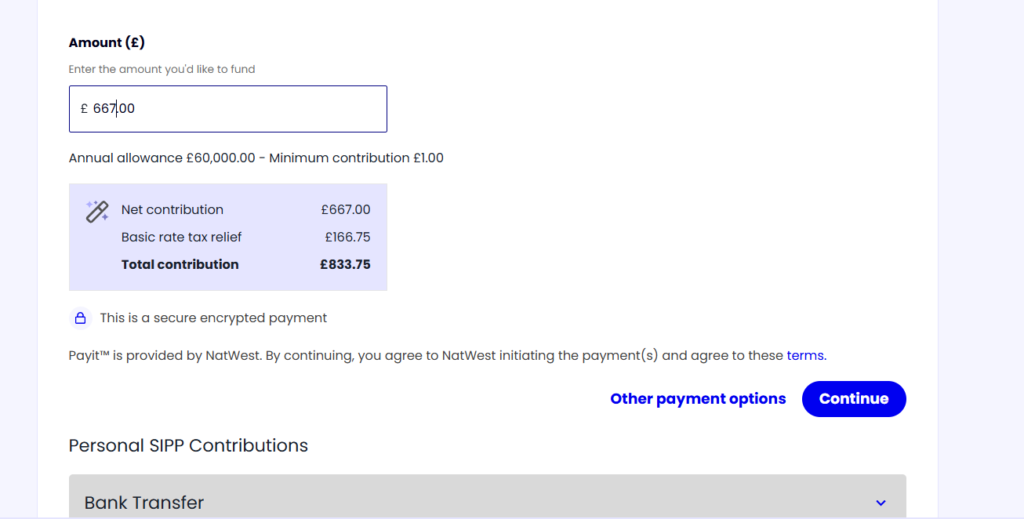

And rather than just tell you, let me show you, from inside my own Interactive Investor SIPP:

That’s a real contribution screen from my own account. I pay in £667, the basic rate tax relief of £166.75 is added on my behalf, and the total contribution landing in my pension is £833.75 . The relief takes 6 to 11 weeks to arrive from HMRC, and then one day the account simply goes up. No forms, no chasing.

Now connect that back to the worked example. The woman who needed roughly £1,200 a month going into her pension doesn’t need to find £1,200 from her own pocket. With basic rate relief, around £960 of her own money becomes £1,200 inside the SIPP. The government funds the rest. For a woman trying to close a retirement gap quickly, that is the single most powerful lever available, and it’s sitting there waiting to be pulled.

The full story of what seven years with a SIPP has actually been like, consolidating old pensions, the locked box mindset shift, the tax relief landing, is in my Interactive Investor Review.

Where to go from here.

Here’s exactly what to do, in order.

- Check your state pension forecast at gov.uk/check-state-pension. Five minutes, and it’s the foundation of everything else.

- Calculate your number using the three step method above. Desired income, minus state pension, times 25.

- Open a SIPP if you don’t have one. The tax relief is too valuable to leave on the table. My Interactive Investor Review covers the platform I’ve used for seven years, my Hargreaves Lansdown Review covers the biggest platform in the UK and my Best Stocks and Shares ISA guide compares the main UK platforms if you want to shop around.

- Start contributing monthly, this month, not next. Even a small amount. The habit and the head start matter more than the size of the first contribution, and if you’re brand new to all of this, my How To Start Investing guide walks you through the groundwork step by step.

The number is calculable. The tools exist. The only step nobody can automate is deciding to begin.

FAQ

How much do I need to retire at 60 in the UK?

More than at state pension age, because your pot funds everything alone until the state pension begins. For a moderate £28,000 a year, that means roughly £385,000 for the years after state pension age plus around £28,000 for each year before it, taking a realistic target to somewhere around £580,000. Retiring at 60 on a lower income target reduces that considerably, so run the gap calculation with your own figures.

How much do I need to retire at 55 in the UK?

Retiring at 55 means funding roughly twelve years before the state pension arrives, which pushes the pot needed for a £28,000 lifestyle toward £720,000. Be aware that pension money usually can’t be accessed before the minimum pension age of 55, rising to 57 from 2028, so a very early retirement also needs accessible savings outside a pension, such as an ISA, to bridge the earliest years.

What is a good pension pot in the UK?

One that covers the gap between the income you want and your state pension, multiplied by 25. For a moderate single person’s lifestyle of around £28,000 a year with a full state pension, that’s roughly £385,000 by state pension age. For a minimum lifestyle it’s dramatically less. There’s no single good number, there’s the number that funds the retirement you’re actually planning.

What is the average pension pot in the UK?

According to the ONS, median private pension wealth is £57,500 among UK adults with pension savings, falling to £19,700 across all adults. FCA data puts the average pot at around £107,300 for people accessing pensions at 55 and over. Most people hold far less than the industry’s headline targets suggest, which is worth knowing before you conclude you’re uniquely behind.

Can I retire on the state pension alone?

The full new state pension pays £12,590.69 a year, which sits below the £13,900 the Retirement Living Standards define as a minimum lifestyle for a single person, and that minimum assumes you own your home outright. So for most people the honest answer is no, not comfortably. Even a modest private pot on top changes the picture meaningfully, which is why starting matters at any age.

Is £300,000 enough to retire on in the UK?

Using the rule of 25, a £300,000 pot supports roughly £12,000 a year of income. Add a full state pension of £12,590 and you’re at around £24,600 a year, sitting between the minimum and moderate Retirement Living Standards for a single homeowner. Enough depends entirely on your housing costs, your lifestyle and your retirement age, so run the numbers for your own situation.

I am not a financial advisor and nothing in this post constitutes financial advice. All investments carry risk and the value of your investments can go down as well as up. Please do your own research and consider seeking independent financial advice before making any investment decisions.

Angelina is the founder of Investing Adventures, where she helps women build confidence with money and investing. With seven years of personal investing experience, she breaks down complex financial topics into practical, actionable advice. Her mission is simple: to help more women take the driver’s seat in their financial future.